EU Green Deal: a brief explanation about the CSRD

Where does the CSRD come from? Who needs to report? What does ‘double materiality,’ ‘supply chain responsibility,’ and ‘stakeholder analysis’ mean within the CSRD? And how do you get started? These are all questions that arise with the arrival of the CSRD. In this blog, we will address these questions and provide you with more insight into this new European legislation.

Where does the CSRD come from?

Europe wants to be a climate-neutral continent, limiting global warming. The EU Green Deal was established to achieve this goal, and the CSRD is a part of that Green Deal. A commonly heard slogan when it comes to reducing CO2 emissions is, of course,”Companies play a significant role”. And although we would prefer it differently, it is true. Companies can truly make a substantial impact.

The CSRD aims to encourage investments in sustainable businesses, allowing them to engage in sustainable innovation. Transparency is a major component in this. Until now, there was little guidance for creating ESG (Environmental, Social, and Governance) reports, making comparisons difficult. The CSRD serves as the instrument for this purpose, because it provides a clearer and more compelling framework for ESG reporting. The difference from previous ways of reporting is that you now also have to demonstrate and substantiate your objectives, and how you intend to achieve them. This transparency is not the only benefit of the new reporting approach; it also establishes a foundation on which to build your sustainable policies.

Who has to report when?

This overview shows you who has to start reporting when:

3 CSRD terms explained

Three often heard terms of the CSRD are:

- Double Materiality

- Supply Chain Responsibility

- Stakeholder Analysis

Double Materiality Analysis

Double materiality analysis examines what your impact on the environment is (impact materiality) and the impact of your environment on you (financial materiality). This analysis shows you which topics you need to report on.

Supply Chain Analysis

The supply chain responsibility is about looking beyond your own actions: What do your suppliers do? What emissions do they produce? How does that impact you? And what improvements can you make in response?

Stakeholder Analysis

In this analysis, you identify which stakeholders may experience significant impacts from your company’s activities, and vice versa. Consider, for example, local residents, your customers or investors.

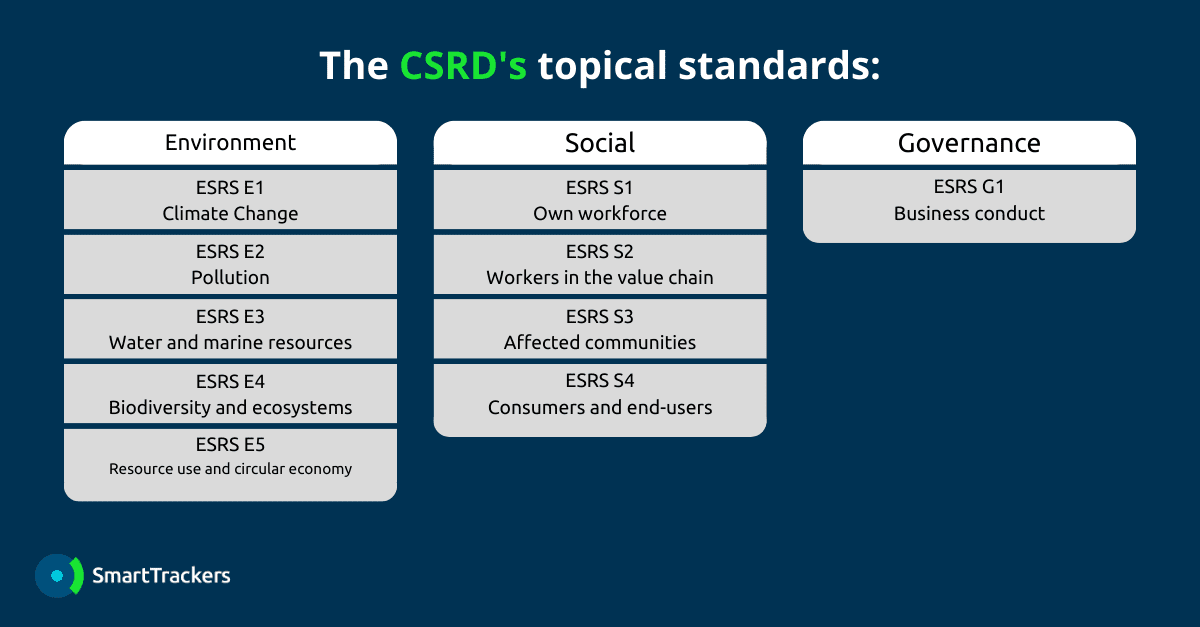

What do you need to report about?

The CSRD has 10 ESG themes, called the topical standards:

For each material theme you must report on your strategy, risk management, policies, measurable goals, action plans, resources, and your KPIs (Key Performance Indicators). Which topical standards are material for you, becomes clear from your double materiality analysis.

How do you get started?

- The first step is to conduct a materiality and stakeholder analysis. You then create a list of potentially relevant topical standards, which you verify with internal and external stakeholders.

- Next, you proceed to identify what you are expected to report on for each theme.

- As a third step, you take inventory of the data you already have on the material themes. This helps you identify your data gaps, which is where you still lack data.

- Afterwards, you start creating action plans to fill those gaps. This marks the start of data collection to comply with the CSRD.

SmartTrackers and the CSRD

We are actively incorporating the CSRD into SmartTrackers, as you can see in our roadmap. We also collaborate with partners who can provide hands-on advice for your company. Do you have any questions about how we can help you? The best step is to request a (free) demo. Feel free to request one here:

Request a demo